Enquiries back on the rise, but firms wrestling with the ‘cost of doing business’, shows latest roofing industry survey

Workloads and enquiries grew in the final quarter of 2022 for roofing and cladding contractors, according to the latest State of the Roofing Industry survey from NFRC and Glenigan, but firms are still grappling daily with high energy, labour and material prices, skills shortages, and late payments.

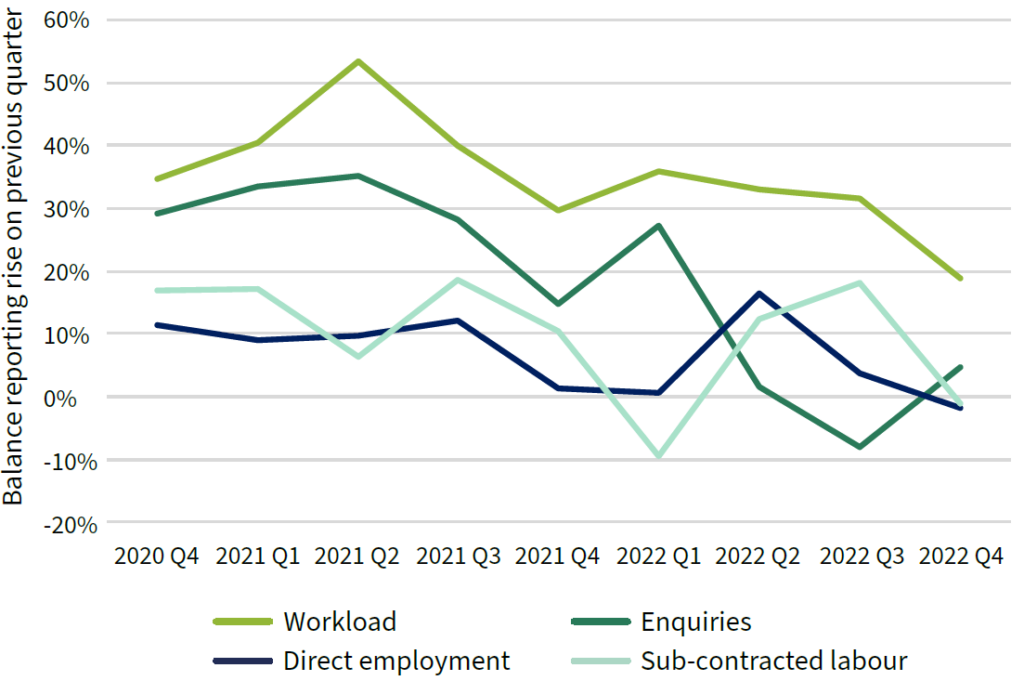

The results of the survey indicate that enquiries rose modestly once again for UK roofing contractors after a slight fall in Q3, with a balance of five per cent of contractors reporting this. (‘Balance’ here refers to the percentage of contractors who reported an increase, minus the percentage who reported decreasing enquiries). Workloads have also continued to grow: 33 per cent of firms saw a rise in workload on the previous quarter, compared to 14 per cent reporting a decline. On the sector level, workload growth was driven by domestic and commercial repair, maintenance and improvement (RM&I) work, whilst a balance of 18 per cent of firms operating in the public non-residential new build market reported a fall in workloads.

Key indicators

Employment levels decreased slightly in Q4, with a balance of two per cent of firms decreasing direct headcount from Q3, whilst a balance of one per cent of firms reduced sub-contracted labour use during the quarter. Despite this slight easing, staff recruitment remains a challenge. 55 per cent of firms reported finding it harder to recruit suitable labour during Q4. Roof slater and tiler was once again the main role that firms were finding it difficult to recruit for (25 per cent).

Material price inflation continued, though at a moderated pace: a balance of 64 per cent of firms report that they paid more for materials during the final quarter of 2022, falling from a balance of 75 per cent during Q3. With the added pressure of wage bills continuing to grow (with increased labour costs reported by a balance of 52 per cent of contractors), the inflated ‘cost of doing business’ has affected tender prices: a balance of 42 per cent of firms raised their prices in Q4.

Other factors that impact firms’ finances stood out from the results of the Q4 survey: firstly, over half of firms (56 per cent) reported that their contractual payment terms were 30 days or less, but only 28 per cent of firms were on average paid within that period. The vast majority of roofing contractors have also seen a sharp rise in their energy costs. 77 per cent of firms reported that energy costs in the fourth quarter of 2022 were higher than a year earlier. Of those firms that reported a bigger bill, the average increase was a sizeable 84 per cent.

James Talman, NFRC CEO, said: “In 2023, firms need support from government to affordably upskill and grow their workforce. The government’s review of payments and cashflow should also examine measures to ensure firms are paid on time (and without funds being unnecessarily held in retention), to allow firms to unlock the cashflow they need to grow their business and invest in skills.“

Allan Wilen, Economic Director at Glenigan, added, “Roofing contractors workload continued to increase, albeit more slowly, during the final quarter of last year. A rise in enquiries supports firms’ expectations of further growth over the coming year.“